Warpaint London PLC: A Growth Story Smoother Than Your Foundation

Warpaint London PLC (AIM: W7L) shows strong earnings growth potential, coupled with high margins, a comfy cash balance, and a debt-free balance sheet.

“Our Mission is to ensure everyone has access to high quality cosmetics at an affordable price.”

Cosmetics producer Warpaint London PLC (AIM: W7L) plans to launch in 400 new stores to bolster its sales and market share. We take a look at management’s growth ambitions and the Company’s financial health against a backdrop of rising costs and supply disruptions.

Paint the town red… or blue… or any colour you want, it’s colour cosmetics after all

Whilst hunting for the next opportunity, like Theseus meticulously navigating the labyrinth in search of the Minotaur, we stumbled upon Warpaint London PLC (the “Warpaint”, “Company”, or “Group”). Whilst meeting our screening requirements1, the Company also meets some of the illustrious Peter Lynch’s rules, namely Rule #1 (“sounds dull, or ridiculous”), Rule #5 (“institutions don’t own it and analysts don’t follow it”), and Rule #12 (“insiders are buyers”). I’ll stop here before this becomes a Peter Lynch admiration post… although, we love you, Peter!

Warpaint offers high quality affordable colour cosmetics under various brand names and operates in the personal care products industry, offering products through wholesale and online channels. More details on product offering and geographic focus in next section.

The Group is currently undergoing its expansion strategy, and given its balance sheet, earnings, and competitive positioning, we believe it still has real upside potential.

Does Warpaint supply face paint for the Navy Seals? Not quite…

Onto the sort of boring stuff. Warpaint was founded in 1992 by Sam Bazini (CEO) and Eoin Macleod (MD), who began by buying and selling close-out and excess stock of cosmetics and fragrances. However, as the Group’s customer base grew so did their desire for a complete range of cosmetics – think Icarus like aspirations with Daedalus’ like wisdom. We have to say that seeing the co-founders continue to run the Company to this day is a positive, especially given their growth track record.

In 2002, the co-founders created the Group’s first own brand named “W7”, after the prefix of the Company’s postcode in West London. This attitude to naming is another green flag, as it shows that the co-founders were more focused on the product than the naming. In 2008, the Group’s focus turned to its own brand offering and by 2016 Warpaint was floating on AIM.

Warpaint has grown mostly organically since the IPO. It did, however, acquire Retra in 2017, which brought the Technic, Body Collection, Man’stuff brands and gifting capabilities to the Group, and Marvin Leeds Marketing in 2018, which brought in-house the Group’s US sales and marketing team – both were all-cash acquisition which we deem as accretive to the Group’s medium and long-term aims.

The Group sells branded cosmetics under the lead brand names of W7 (55% of sales) and Technic (36% of sales). W7 is sold in the UK primarily to retailers, and internationally to local distributors or retail chains. Technic is sold in the UK and continental Europe with a significant focus on the gifting market, mainly for high street retailers and supermarkets. Warpaint also supplies own brand white label cosmetics produced for several major high street retailers. They also sell under their other brand names of Man’stuff, Body Collection, and Chit Chat.

The key thing here is that Warpaint provides a complete end-to-end product offering everything, from foundation, bronzer, eye-shadow, and false nails to brushes, lip gloss, beard oil, shampoo, and shower gel. The focus on colour cosmetics has allowed Warpaint to establish a strong presence in the personal care products industry, particularly with the 16-34 age demographic.

The Group has also created a pipeline of future customers via its Chit Chat brand. Chit Chat is aimed at pre-teens and offers a wide range of cosmetics, accessories, and toiletries, which are all pocket money friendly. These products make an ideal gift set for any pre-teen looking to experiment with colour cosmetics for the first time before graduating to the big leagues of W7 and Technic. You can now go full glam without spending too much of your weekly allowance.

The Company provides the aforementioned products through wholesale channels, retailers, distributors, retail chains, and online platforms. It operates in multiple regions2, including:

United Kingdom (43%)

Denmark (20%)

Spain (13%)

United States (8%)

Australia & New Zealand (2%)

Rest of Europe (11%)

Rest of World (2%)

Having established itself in the off-price market, just as the world was coming to a slowdown in 2020, the Group launched into full price retail with Tesco and Wilko, and Boots in 2022. Warpaint began selling on Amazon (US) and its own website in 2020, resulting in 24% YoY sales growth – this strategic e-commerce expansion is what we see as yet another green flag.

Growth, growth, growth

Onto the not so boring stuff. The Group’s strategy consists of six key pillars but we only care about two:

Grow market share in the UK

Grow market share in the US and China

Warpaint has shown great ability to expand its market share and product presence. Despite only launching in 54 Tesco stores in 2020, Warpaint is now available in more than 2,0003 stores in the UK, with

more to come. During an unscheduled trading update in 4Q23, management stated that the sales pipeline is increasingly robust almost doubling store presence in both CVS (US, 372 stores) and Boots (UK, 102 stores). These new stores followed a successful W7 product launch in 400 Etos stores (Netherlands) and 100 Watsons stores (Philippines).

What’s interesting is that the Company has not used any mass market TV or radio advertising – which makes sense given the target audience and their preference for TikTok dances. The Company does not have a set marketing campaign and instead consider each marketing initiative on a case-by-case, ROI basis – like music to an investors ear. Warpaint has done well by using genuine TikTok and Instagram make-up influencers and brand ambassadors to ensure a high penetration rate.

Rather than spending money on traditional advertising, Warpaint deploy their cash prudently. To ensure the success of their expansion strategy, the Company uses its cash to buy and hold a lot of inventory. This allows them to always have a full range of colour cosmetics available to deliver to new and existing customers. Inventory availability is a key benefit as it allowed the Company to shield itself from all the supply disruptions that took place during 2021/22 and continue to cause issues. This prudent inventory management enabled Warpaint to secure stock prior to costs rising and expand its profit margin.

Warpaint has also simplified its product range - yet another positive. Over the last few years, the Company has reduced its brand and product offering foregoing large product development costs. This has been particularly beneficial in the gifting business which discontinued products every two years. We view Warpaint’s five brand offering as a big bonus that will enable it to penetrate markets faster and easier than before.

Warpaint’s arsenal

Since its inception, Warpaint remains focused on its gross margin, cash generation, and strong, debt free balance sheet. This, in our opinion, is one of its key strengths.

In an environment of rising capital costs, Warpaint has been able to avoid interest payments by simply being debt free. This is achieved by outsourcing manufacturing and ensuring an asset light structure.

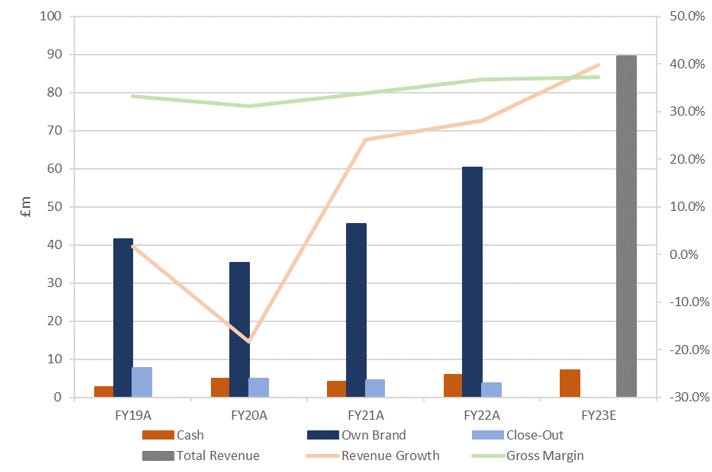

Sales have increased YoY at an annual rate of 8.9% for the past five years representing the strong demand for Warpaint’s product offerings. Operating expenses are relatively fixed, and costs are tightly controlled – as you would expect of an affordability focused firm. Warehouses and offices are leased4, meaning that capex is immaterial and mainly relates to in-store display furniture. This is provided free of charge to B2B customers if they purchase sufficient inventory.

The focus on costs has allowed the Company to increase profit margins over the last three years from 31% to 37% in FY22. More importantly, as a result of effective cash management, Warpaint has been able to reduce its cash conversion cycle by an average of 12.5% each year to 205 days between FY20 and FY22. The Company’s ability to generate and receive cash is key to its growth, and we would like to see the cash conversion cycle further reduce to the mid-100s. We can expect this to happen as the Company captures more market share and is able to better negotiate its receivables and payables. A further testament to Warpaint’s product demand can be seen in its reduction in inventory days. Over that last three years, Warpaint has been able to reduce its inventory days by 36, down to 165.

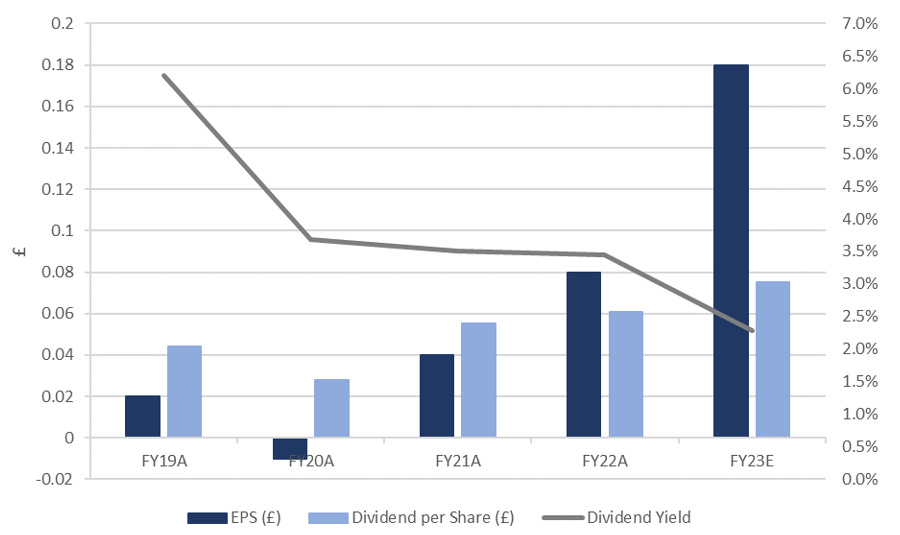

Despite the Group not having a defined dividend policy, the five-year average dividend yield and pay-out ratio are 3.8% and 86.5%5, respectively. Truth be told, our investment thesis does not rely on dividend income but if management can’t find a better use for cash and don’t want to overexpand or acquire inappropriate targets, which we strongly agree with, then we’ll gladly accept the dividends.

Another strength is that the insiders are buyers, in fact 51% is owned by the co-founders. Whilst this does reduce traded volume, it does ensure that there is no divorce between ownership and control. It also ensures that management do not overexpand or overpay for acquisitions as their capital is also on the line. In fact, more than 75% of the CEO’s total compensation is performance or company stock related. Taking into account that Warpaint is the co-founders’ brainchild and their total comps are linked to its performance is quite comforting, as you can imagine.

Additionally, and as expected of small/mid cap UK equities, the Company does not receive a lot of Analyst coverage. We note that Shore Capital and Hybridan appear to be the only ones covering the stock, albeit Shore Capital is also the nominated Adviser and Broker. We believe that such a lack of Analyst coverage is beneficial to our investment thesis as it allows us to get it before the big equity houses.

Without making this section too number focused, our blended target price6 is GBX 549 resulting in a c.45% upside to February 1st close. This utilises a WACC of 8%, long-term growth rate of 2.5% and EV/EBITDA multiple of 13.5x. Alongside some other marginal improvements in margins, and net working capital.

Does anyone have a beauty blender? I may have made a mistake

With every investment thesis we also must consider potential risks that may prevent the Company from reaching its potential.

Anytime we discuss expansion strategies we have to be cautious about which markets and geographies we are moving into. Therefore, a risk here is that the Company gets a bit too excited and overstretches itself without waiting for the appropriate data to come through. Expansion can be expensive, and inappropriate expansion can be detrimental to a company’s performance. That being said, management have shown that they are not trigger happy and instead carefully calculate their plans.

Another key risk, especially when combining excess cash and expansion strategies, is overpaying for dilutive acquisitions. This is particularly prevalent when companies try to enter new geographies by purchasing an existing customer base. Whilst this could pay off, quite frequently this strategy results in goodwill right-downs and future divestments – and M&A bankers are the real winners. Warpaint has shown great restraint in non-core acquisitions and therefore, we are not concerned about acquisition risks.

One could argue that Sam and Eoin are Warpaint, and that’s a bit of a risk. Both have been working since their late teens and are now in their early 60s, so surely at some point they’ll take a back seat and enjoy the fruits of their labour. New management, especially one which hasn’t been cultivated by the Company, could be a laggard to the expansion strategy. At the moment, this is not a key risk although we’ll have to closely monitor their succession planning.

There are also risks outside of the Company’s control. Currently these are interest rate risk and supply disruptions. Increasing interest rates have been accretive given the Company’s focus on affordable colour cosmetics, however, as rates come down and disposable income increases there is a risk that demand for affordable products will wane. That being said, the Group has a sticky customer base particularly due to its target age group – I don’t know any teens with mortgages.

Supply disruptions are a key risk for any physical goods company, but Warpaint’s prudent inventory management has mitigated this risk so far. With further geographic expansion it will be interesting to see how the Company deals with local distribution centres.

A final, blue sky thinking risk of any small/mid cap company is that it gets acquired by a larger player at a price that is not truly reflective of its growth capabilities. This ultimately strips shareholders of potential value. However, we do not foresee the co-founders selling out their brainchild just yet.

Don’t distract me, I’m applying setting spray

Overall, Warpaint’s balance sheet remains strong and with the financial resources to support its medium to long-term growth ambitions. We are excited to see the Company realise its potential. The Group’s ability to grow revenue, margins, cash, and market share, despite an inflationary environment is also comforting. We are supportive of the Group’s growth strategy and the subsequent tailwinds to earnings. We now sit back and observe Theseus approach the Minotaur…

(i) little/no debt, (ii) high gross/EBITDA margin, (iii) strong revenue/earnings growth, (iv) healthy cash position, (v) market cap < £300m.

% of Group sales.

Own estimate from FY22 earnings call (1,400 stores) and subsequent trading updates.

Note for us accounting geeks: As you’ll know, following the introduction of IFRS 16, costs with operating leases previously recognised as an operating expense are now recognised through interest payments and depreciation, i.e., below EBITDA thus enhancing margins.

Excluding FY20 where the Company paid out £0.061/per share despite having negative net income.

Gordon growth and multiples approach.